For most of the last decade, Navi Mumbai was Mumbai’s pressure valve — the place buyers went once South and Central Mumbai stopped making financial sense. That’s no longer the full picture. In 2026, parts of Navi Mumbai property rates in line with established Mumbai suburbs, while other nodes are still playing catch-up to infrastructure that’s already built and operating, not just promised.

That gap — between where prices are and where the underlying infrastructure says they should be — is where most of the genuine opportunity in this market still sits. Here’s where things stand, node by node, and what’s actually moving the needle.

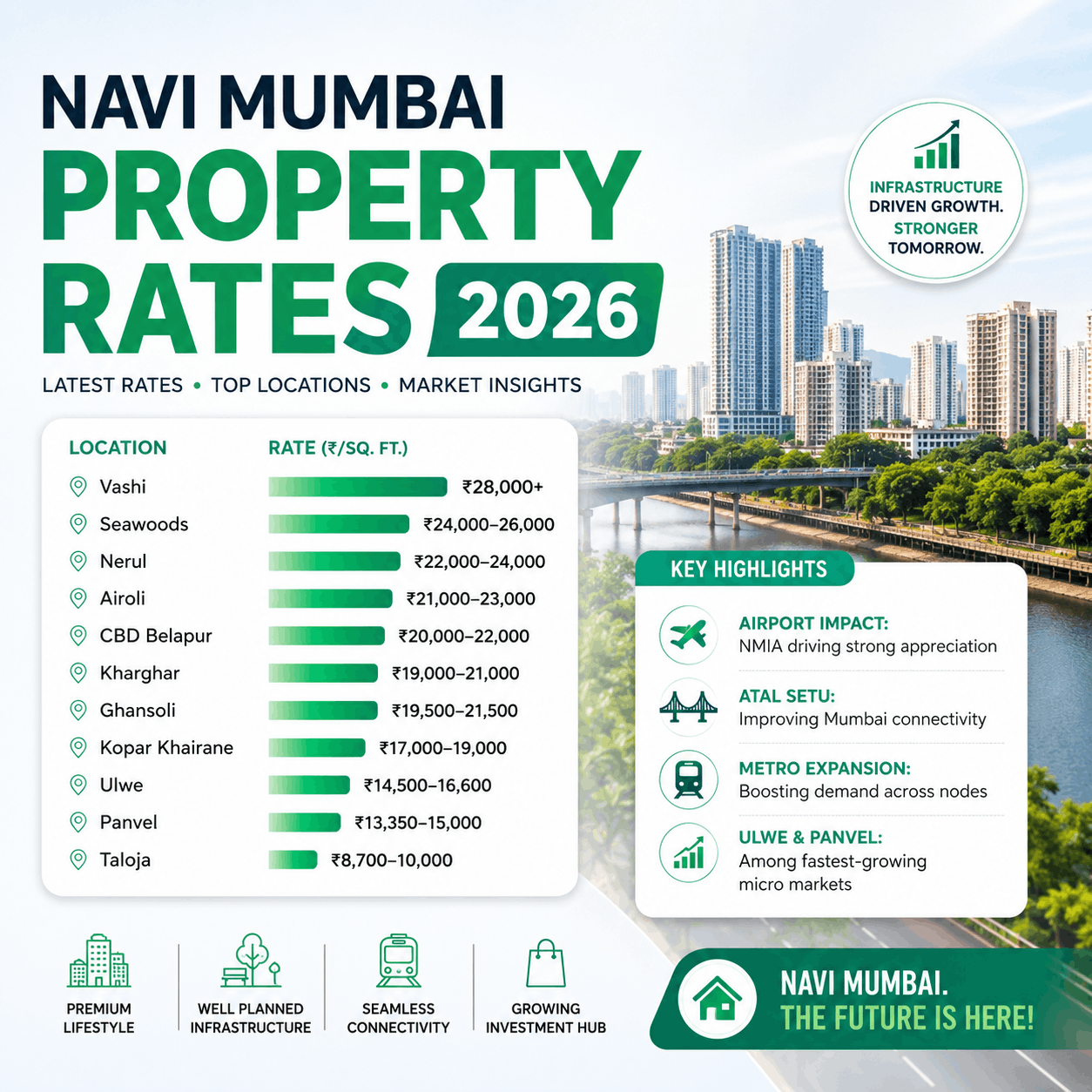

Summary

Residential rates across Navi Mumbai currently span roughly ₹6,000 to ₹29,000 per square foot, depending entirely on the node. Growth in the emerging corridors has run between 8% and 15% year-on-year — a pace backed by real, operating infrastructure rather than speculation: a metro network that’s now partly functional rather than perpetually “upcoming,” the Mumbai Trans Harbour Link cutting cross-harbour travel from over an hour to about 20 minutes, and an international airport that has moved from rumour to final-stage construction.

- Airport Impact: NMIA driving strong appreciation

- Atal Setu improving Mumbai connectivity

- Metro expansion boosting demand

- Ulwe & Panvel among fastest-growing micro markets

Navi Mumbai Property Registration

Asking rates rising is one thing; transactions are the real tell. Mumbai Metropolitan Region registrations hit a 13-year high in April 2026, crossing 12,000 units in a single month, with stamp duty collections of over ₹1,100 crore — up 5% on the year before. Navi Mumbai’s share of that volume has been climbing steadily, driven by a combination of improving connectivity and a price gap with the island city that, while narrowing, hasn’t closed yet.

Navi Mumbai Property Rates Area-Wise 2026

| Area | Price Range (₹/sq.ft) | YoY Movement | What’s Driving It |

|---|---|---|---|

| Taloja | ₹6,500 – ₹9,000 | ▲ ~15% | Lowest entry point in the region; Metro Line 1 now operational |

| Kharghar | ₹11,000 – ₹18,000 | ▲ ~12% | CIDCO-planned layout, active ICP Phase 1 bidding, metro access |

| Ulwe | ₹11,500 – ₹14,000 | ▲ ~14% | Airport-adjacent node, direct MTHL beneficiary |

| Panvel | ₹9,000 – ₹12,000 | ▲ ~10% | Affordable-to-premium mix, education hub, MTHL-connected |

| Nerul | ₹14,000 – ₹22,000 | ▲ ~9% | Mature, sea-facing stretch along Palm Beach Road |

| Seawoods | ₹20,000 – ₹29,000 | ▲ ~10% | Premium hub anchored by Seawoods Grand Central |

| Dronagiri | ₹6,000 – ₹7,500 | ▲ ~8% | Port-economy linked, longer-horizon bet |

A quick read on this table: Taloja and Dronagiri are where first-time buyers and tighter budgets still find room. Kharghar and Ulwe are the contested middle ground — both growing fast, both arguably still under-priced relative to their infrastructure. Nerul and Seawoods are where the froth has already settled; you’re buying maturity, not upside.

Factors Driving Property Prices in Navi Mumbai

1. Infrastructure has stopped being a pitch line.

The MTHL connects Sewri to Chirle in roughly 20 minutes — a number that shows up directly in Panvel and Ulwe pricing today, not in some hypothetical future. Metro Line 1, running Belapur to Pendhar, is fully operational and has visibly shifted buyer sentiment in Kharghar and Taloja. The airport itself, after years of “any day now,” is now in its final construction phase — and the market has quietly started pricing it as a near-certainty.

2. Rental yields

Rental are climbing alongside capital values — which doesn’t usually happen together. Kharghar is delivering yields around 3.4%; Ulwe and Taloja have edged up to nearly 3.8%. For an MMR market where yields have historically stayed compressed below 3%, that’s a meaningful shift, and it suggests the rental market is validating the price growth rather than lagging behind it. A 2 BHK in Panvel currently rents for ₹12,000–₹20,000 a month.

3. Ready reckoner rates haven’t caught up to the market

Comparing government circle rates to actual transaction prices is one of the more underused exercises a buyer can do, because the gap tends to predict where future reckoner revisions land.

| Location | Rate Per Sq. Ft (PSF) |

|---|---|

| Vashi | ₹28,000+ |

| Seawoods | ₹24,000–26,000 |

| Nerul | ₹22,000–24,000 |

| Airoli | ₹21,000–23,000 |

| CBD Belapur | ₹20,000–22,000 |

| Kharghar | ₹19,000–21,000 |

| Ghansoli | ₹19,500–21,500 |

| Kopar Khairane | ₹17,000–19,000 |

| Ulwe | ₹14,500–16,600 |

| Panvel | ₹13,350–15,000 |

| Taloja | ₹8,700–10,000 |

In Ulwe, Taloja, and Panvel, market prices are already running 40–80% above their reckoner valuations. When that gap gets that wide, a reckoner hike usually isn’t far behind — which has direct stamp duty implications for anyone planning to buy in the next cycle, not just a curiosity for analysts.

How to Know Navi Mumbai Property Market Trends

Three filters separate buyers who do well here from buyers who get lucky:

- Who else is in the room? When local end-users, investors, and NRI buyers are all converging on the same node — true of Ulwe and Kharghar right now — that convergence is itself the signal. It means demand isn’t coming from one narrow segment that could exit all at once.

- What did the last three years actually look like, not the last three months? A single quarter of strong numbers doesn’t tell you much. Steady, multi-year appreciation is a different story than a spike.

- Has today’s price already absorbed tomorrow’s story, or is there room left? Taloja, priced well under Nerul, is arguably earlier in its curve — its metro connectivity only recently went live. Nerul’s premium, by contrast, is largely already priced in; you’re not buying a re-rating, you’re buying stability.

Nodes of Navi Mumbai

Taloja — Metro Line 1 is live, the reckoner sits at ₹56,100/sq.m, and RERA-approved launches like Naman Platina are transacting around ₹8,250/sq.ft. This is the node where the infrastructure-to-price gap is widest.

Ulwe — A CIDCO-planned airport node with both MTHL access and the Nerul–Seawoods–Belapur rail corridor working in its favour. Circle rate of ₹58,800/sq.m against a market range of ₹11,500–₹14,000/sq.ft tells you most of what you need to know about where this is headed.

Kharghar — The most “arrived” of the emerging nodes: strong liveability, mature social infrastructure, and consistent appreciation. Currently ₹11,000–₹18,000/sq.ft, supported by metro access, active ICP bidding, and proximity to the airport corridor.

The Bottom Line

There’s no single breakout location in Navi Mumbai this year — that’s the real story. It’s infrastructure translating into pricing across several nodes simultaneously, at different stages of the same curve. Kharghar already had its “undervalued” moment a few years back. Whether Ulwe or Taloja are having theirs right now is the more useful question for anyone deciding where to put capital in 2026 — and it’s a question worth answering with site visits and RERA checks, not just a rate table.

FAQs for the Navi Mumbai Property Rates

Q. What is the average property rate in Navi Mumbai in 2026?

There’s no single citywide average worth quoting — rates range from roughly ₹6,000/sq.ft in Taloja and Dronagiri to ₹20,000–₹29,000/sq.ft in Seawoods. The node matters far more than any blended average.

Q. Which area in Navi Mumbai is most affordable to buy in right now?

Taloja and Dronagiri remain the cheapest entry points, both under ₹9,000/sq.ft. Taloja has the edge since Metro Line 1 is already operational there.

Q. Which Navi Mumbai locations are seeing the fastest price growth?

Taloja (~15% YoY) and Ulwe (~14% YoY) are leading, both on the back of infrastructure that’s now actually functional — metro connectivity in Taloja, MTHL access in Ulwe.

Q. Is Ulwe still worth buying into, or has the price already run up?

Market prices in Ulwe already sit well above the reckoner rate, meaning a fair share of the airport-led upside is priced in. It’s still appreciating, but project-level due diligence now matters more than the broader location story.

Q. Why do Navi Mumbai’s reckoner rates look so much lower than market prices?

Reckoner rates are revised periodically and tend to lag fast-moving markets. In Ulwe, Taloja, and Panvel, actual prices run 40–80% above reckoner values — usually a sign that a rate revision is overdue, not that the market is mispriced.

Q. Should I buy ready-to-move or under-construction in Navi Mumbai?

Depends on risk tolerance. Under-construction in Taloja or Ulwe offers better entry pricing but carries possession-timeline risk. Ready-to-move in Kharghar or Nerul costs more but removes that uncertainty.

Q. Are property prices in Navi Mumbai negotiable?

Yes, especially on under-construction and newly launched projects, where developers have more room to flex. That room shrinks as a project nears possession or sells out.

Q. Is the airport the main reason prices are rising, or is something else driving it too?

The airport gets the headlines, but Metro Line 1 and the MTHL have independently moved pricing in Kharghar, Taloja, and Panvel — areas that aren’t even directly adjacent to the airport node.

Q. How do rental yields in Navi Mumbai compare to capital growth?

Yields are rising alongside prices, not lagging behind them — Kharghar is around 3.4%, Ulwe and Taloja near 3.8%. That’s unusually strong for MMR, where yields are typically compressed.

Q. Which node is best suited for NRI buyers?

Ulwe, Seawoods, and Kharghar see the most NRI interest — mainly for resale liquidity and infrastructure certainty rather than speculative upside.